The U.S. economic climate, commercial deposit and lending companies, and the outlook for business serious estate financial loans topped the agenda at CU Small business Group’s (CUBG) 2021 Countrywide Organization Companies Conference.

Larry Middleman, president/CEO at CUBG, a CUNA affiliate organization member at the associate degree, delivers some highlights from the occasion.

CUNA Information: What were some of the huge discussions in the course of the meeting?

Larry Middleman: Mike Schenk, CUNA’s main economist, gave fairly a beneficial outlook on the economic system in common. We also listened to from Dianne Crocker of LightBox on the forecast for professional genuine estate (CRE), which proper now demonstrates several sectors are undertaking incredibly perfectly.

Hospitality and business office industries have bounced back again nicely just after big drops in 2020.

Yet another very hot subject was how to get branches a lot more involved in industrial lending. Dana Gray of BECU in Tukwila, Clean., spoke on how the credit history union has applied professional financial loan experts in their branches to bridge the regular gap among the central business lending area and the branch network.

There was also much dialogue about making use of know-how to greatly enhance performance in the commercial lending place via industrial financial loan origination methods, which make conclusion-to-conclusion processing more efficient.

Furthermore, there was some terrific dialogue all over providing lending and deposit services to non-gains in your neighborhood, anything definitely at the heart of the credit history union mission.

Q: What were being some other highlights?

A: Our discussions with credit history unions in advance of, through, and immediately after our occasion proceed to reveal that business loan systems are not just surviving the pandemic, most are flourishing.

Lending action concerning credit score unions and CRE investors is very powerful. Overall, professional personal loan balances have increased in spite of the pandemic, and the same goes for professional deposit balances.

Click to enlarge. Whole industrial share deposits.

Industrial deposits rose close to 50{ac23b82de22bd478cde2a3afa9e55fd5f696f5668b46466ac4c8be2ee1b69550} in 2020 and one more 15{ac23b82de22bd478cde2a3afa9e55fd5f696f5668b46466ac4c8be2ee1b69550} so far by means of June 30, 2021.

Paycheck Protection Plan (PPP) lending has lifted recognition of and fascination in Smaller Business enterprise Administration (SBA) lending courses. Lots of credit unions are contemplating increasing over and above traditional loans into SBA lending.

Q: What are the greatest company lending options right now?

A: Three spots stand out as the biggest parts of option now:

- Producing courses for processing smaller loans proficiently. This style of lending is the heart and soul of helping modest enterprise users in any credit score union.

- Implementing a official financial loan origination process to assist and regulate the industrial lending system from conclusion to stop.

- Expanding into SBA lending making use of the momentum the PPP has generated.

Q: What are your largest worries associated to organization lending?

A: Credit rating unions are going through a couple of significant difficulties proper now.

Very first is the problems of obtaining, employing, and retaining professional business workers. Credit score union bank loan volumes are bigger than at any time, and it is a substantial obstacle to recruit and keep the appropriate workers to aid operations.

2nd, the low-fascination-fee surroundings is difficult for credit score unions as borrowers want to lock in low prices for lengthy conditions, these kinds of as a 10-12 months fixed-amount commercial loans. This offers a challenge for asset/legal responsibility administration in credit rating unions, where the wish is to originate loans with shorter fixed-rate conditions, this sort of as 5 years.

Ultimately, an overriding concern is how to hold loans and finally grow the professional portfolio. Debtors are refinancing and consolidating loans at today’s quite favorable prices and conditions.

Some credit unions have to make 15-20{ac23b82de22bd478cde2a3afa9e55fd5f696f5668b46466ac4c8be2ee1b69550} portfolio advancement just to offset runoff from loans exiting for these motives.

Q: How are your clientele addressing organization lending dangers associated to COVID

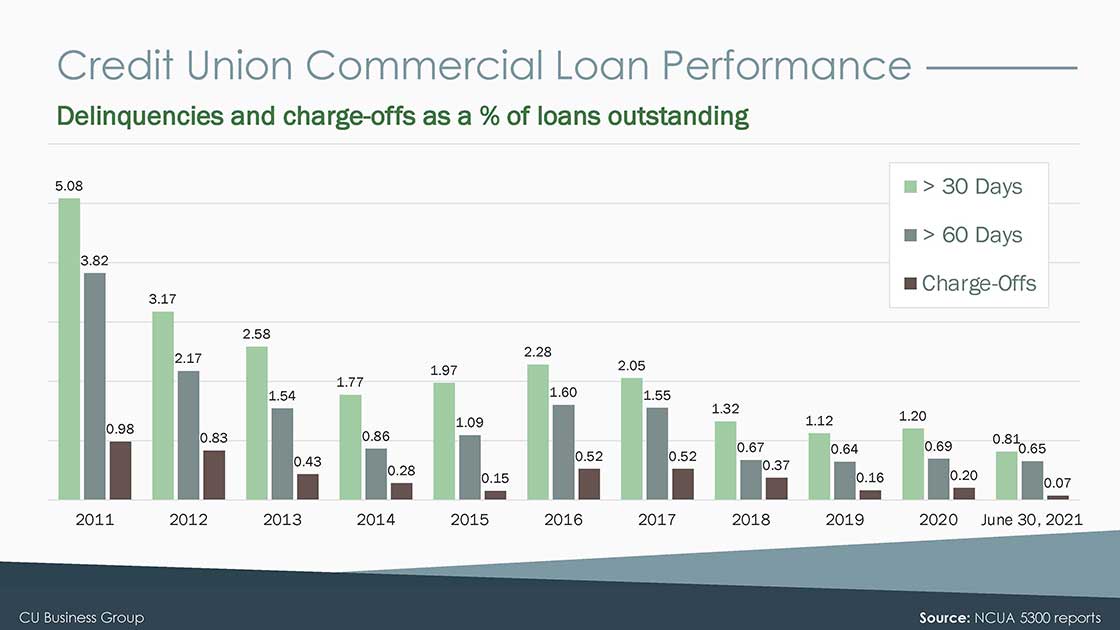

A: There carries on to be uncertainty, but so considerably credit history unions have escaped from any major bank loan losses or dilemma financial loan difficulties. The June 30, 2021, NCUA figures bear this out.

Simply click to enlarge. Credit union business personal loan overall performance.

1 session at the conference delved into how credit score unions are addressing COVID-distinct challenges these kinds of as collateral valuation, existing personal loan-to-price ratios, and many others., furnishing a blueprint for how to assess loans and collateral presently in the portfolio that may perhaps be undergoing pressure.

As are the standard traits currently, quite a few of the meeting displays talked over the need for greatest-in-course digital expert services, remote obtain, and the gains of cloud computing. What utilized to be “fancy cellular technology” is now regular in day-to-day operations.

Q: What is the CRE outlook in the coming months?

A: Credit score unions have truly recognized them selves as a feasible option for industrial financing and depository solutions. Refined commercial real estate traders are constantly hunting for more lending resources, and credit history unions are now in that mix.

The forecast for CRE is really rosy for the in the vicinity of potential. The sectors which have been toughest strike by the pandemic—hospitality and office—have rebounded and are creating a sound comeback. The industrial, producing, and self-storage segments are doing perfectly and had been not truly impacted by COVID.

Q: What had been some essential takeaways/insights from the convention?

A: A person major lesson was finest methods in placing up and organizing the industrial spots: profits, company, underwriting/credit rating, deposits, branches.

Credit rating unions are hunting to diversify outside of CRE. There was superior curiosity in items these kinds of as SBA loans, smaller financial loans, treasury products and services, and so forth., all of which deliver upcoming growth chances.

Credit unions also need to have a range of resources for bank loan growth. These include things like shopping for participations and using 3rd functions these as CUBG to supply, approach, and originate loans.

Q: Is there something else you’d like to incorporate?

A: Attendance at CUBG’s countrywide organization providers conferences proceeds to increase quickly. This was our 15th 12 months keeping a countrywide conference, and attendance has risen from less than 100 men and women in the early yrs to extra than 700 at our 2021 virtual function.

This definitely illustrates the interest credit history unions have in aiding smaller corporations and diversifying their financial loan portfolios.